Ethereum will become an effective conduit for short-term consumers and money-making until the issues of high gas taxes and network solutions can be resolved entirely. The competitive benefit of MDEX, a DEX that serves all shared exchange chains. MDEX’s TVL has crossed 5.2 billion dollars quickly since launching at BSC on 8 April and is the largest daily trading volume above 5.1 billion dollars. After its publication, this article examines MDEX’ results highlights.

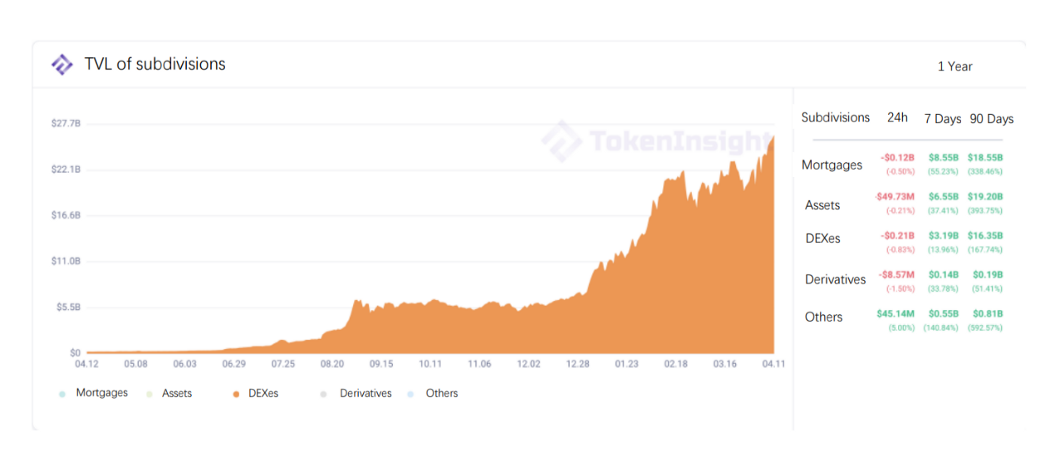

In 2020 Q2, in the blockchain market, DeFi innovation is fast emerging. The most famous trade among them was decentralized exchange (DEX). The new DEX TVL is over $20 trillion, according to TokenInsight, first of all DeFi programs.

MDEX obtained the TVL more than US$5.2 billion since launching on BSC

MDEX (Huobi-Eco Chain), focused on an automated marketing manufacturer (the ‘AMM’), is a decentralised exchange network on HECO. Listed at BSC on April 8, the company constitutes one of the few decentralized exchanges in the dual chain industry. The cost of HECO and BSC is much more efficient, reflecting a distinct benefit compared to the expensive transaction fees for Ethereum. BSC and HECO now have access to DeFi for retail consumers. MDEX implements the “dual mining” mechanism, in addition to utilities such as transactions and staking.

Investors can participate in the liquidity pool for obtaining mining revenue, i.e., “liquidity mining,” and in MDEX token transactions for obtaining mining earnings, i.e. “transaction mining,” token transactions.

In January 2021, MDEX was listed and since then a significant transaction size has been reached. Particles of interest are MDEX’s 24-hour trading rate, which rates above Pancake and Uniswap, since its launch at BSC on 8 April 2021.

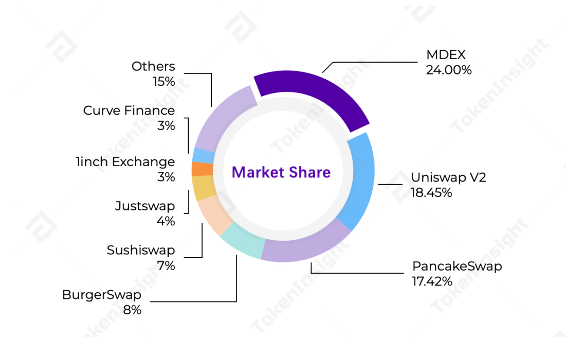

The 24-hour number of MDEX trades hit USD 1,912, with a combined market share of 23.54 percent briefly ranging first on the DEX market, according to Coinmarketcap, as of April 19, 2021.

MDEX will also be eligible for cross-chain purchases with digital assets on other public chains, in addition to BSC and Ethereum.

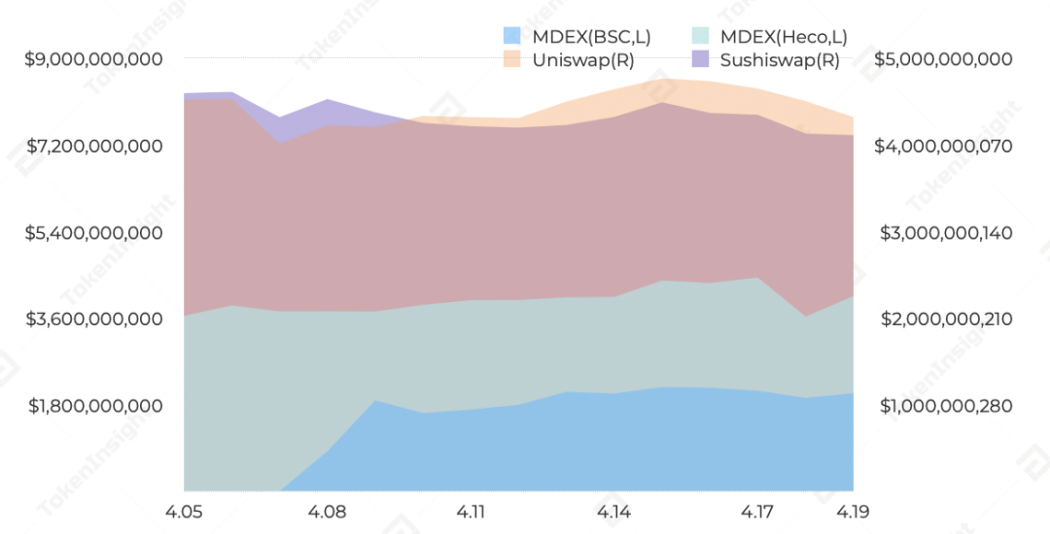

The lock-up amount of MDEX in BSC has risen to US$2.16 billion since its listing at BSC, and stabilized at approximately US$2 billion.

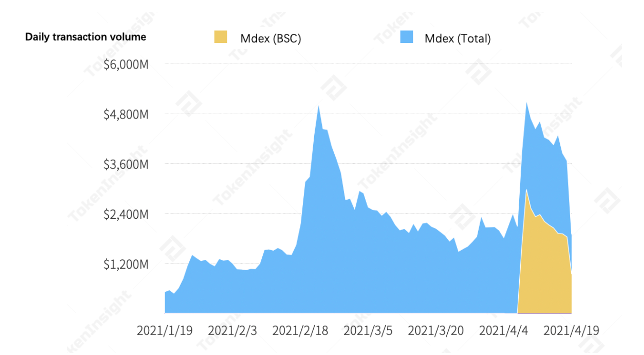

MDEX’s TVL increased to 5.2 billion dollars (April 13), then stabilized to about 4 billion dollars, and on April 9 it again grew to 2.98 billion dollars and stabilized over 1.8 billion dollars with the exception of April 19.

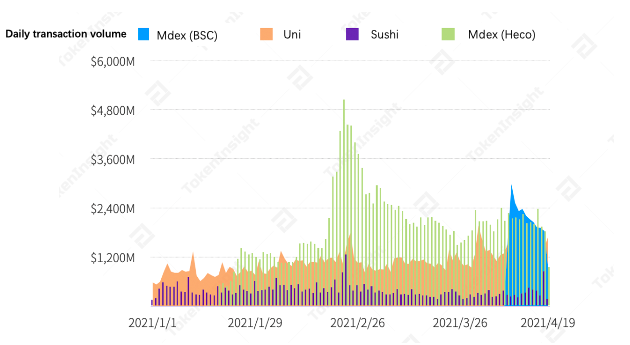

The new DEX transaction volume data shows clearly that MDEX has hit record levels of $ 5.05 billion in daily transaction volume since it was launched (February 22). For BSC in MDEX, the BSC has seen a daily turnover of nearly $3 billion (April 9: $2,978 billion) in its maximum daily transaction volume. Overall, HECO and BSC together earned the largest regular transaction value of US$ 5 124 billion (April 9).

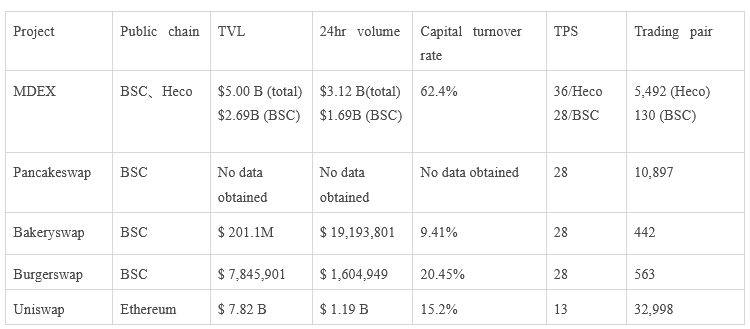

As seen in the following table, TokenInsight has compiled new DEX results. While MDEX lists only more than 130 trading pairs, its turnover amounts to 62 per cent, and its volume of transactions is the highest among many DEXs.

Its hyperactivity is caused by its special mechanic’s great mining inspiration. The day that BSC was launched, a number of successful trading pairs, such as WBNB/MDX, had the highest instantaneous mining income at 1,9 million per cent, but such a strong turnover lasted just 15–30 seconds. After the influx of many customers, APR eventually fell to thousands.

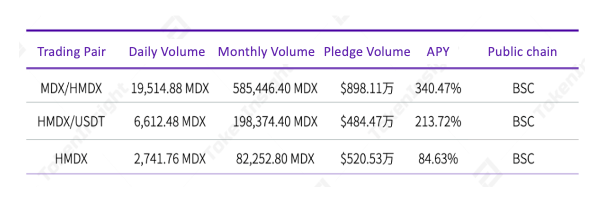

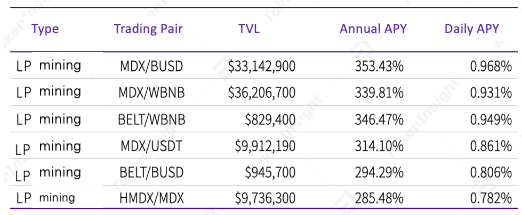

The latest mining data on the BSC chain are collected and arranged in the following table. The top six liquidity mining returns stay steady at about 300%.

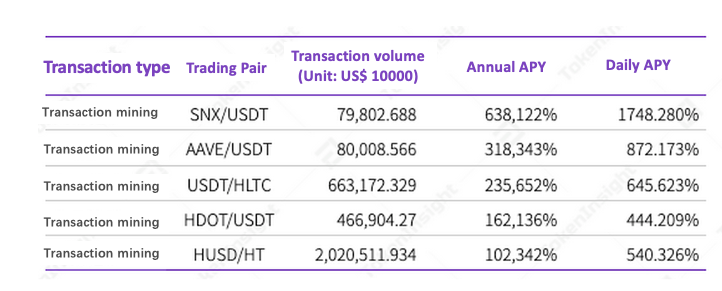

The highest APY (currently SNX/USDT) can still be above 1500 per cent for transactions mining data (both HECO and BSC), and the daily APY of the top 12 trading pairs are still around 124 per cent or more stable.

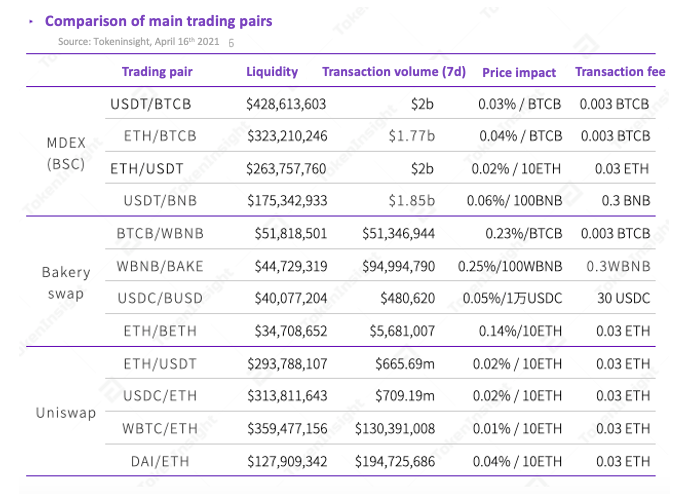

In three exchanges, MDEX, Bakeryswap and Uniswap, TokenInsight compared the four best liquid trading pairs. The competitive advantages of slippage are easily recognizable in the MDEX liquid trading pair. There are just a few extremely liquid trading pairs that MDEX deploys on the BSC. The ‘price effect’ column in the table should be defined as the product of measurement by using the number of denominators for each DEX trading pair. You would likely get 0.06% slippage when resetting 100 BNB for the MDEX US$T/BNB trading pair. The estimation of the transaction charge therefore uses the same share of transactions as the column of price impacts. For example a transaction fee of around 0.3 BNB is needed to replace 100 BNB for MDEX’s US$T/BNB transaction pair.

Cross-chain mining: a potential revenue stream

MDEX cross-chain mining process is a distinct feature in comparison to other DEX spot resources programs. Since various public chains are separate and MDEX are parallel to each other in several public chains, interoperability with each other is complicated, meaning that the reliability of the use of assets is comparatively limited. It must then overcome the liquidity of cross-chain assets for MDEX that cross chains.

The MDEX scheme is pretty straightforward and simple: cross-chain mining.

Both BSC and HECO MDEX have deployed DEX. The Ethereum Network has also deployed a mapping server to temporarily direct HECO traffic to the DEX. Please notice that MDEX is not accessible at Ethereum at this time.

It is also worth noting that HMDX in BSC is a HECO chain MDX mapping asset acting as a BSC to HECO cross chain asset. Users will pass HECO’s MDX to the BSC chain via the cross-chain bridge as HMD, which is traded with the BSC chain ratio of 1:1 to MDX. Or the BSC chain can be used by users directly using HMDX.

The cross-chain bridge supports in addition to HMDX cross-chain properties, such as Tribe and FEI, to be listed on the Ethereum Network after the launch of MDEX.

Users will receive additional mining revenue in different ways through MDX/HMDX and HMDX/US$T trading pairs:

– You can start secondary mining through the mining pool on HECO when you exchange the MDX from BSC to HMDX

– By stacking the MDX (made on the chain of BSC) or USDT for mining on the chain of BSC, you can get MDX on the BSC chain and swap it to the He network for mining, or swap it to USDT for profit;

– MDEX offers a single token of the BSC chain HMDX mining pool for users. Users can pledge MDX in the HECO chain in order to get MDX of the BSC chain, but the revenue is below the initial two. After receiving MDX, users can also decide to use the BSC network mine.

Since the BSC’s network mining revenue is relatively high (the annualized MDX / USDT trading couple in the BSC network are up to 376,92%), users always want to mine or exchange HMDX for MDX, then mine MDX on their BSC chain. DEX gains liquidity in BSC while at the same time combining liquidity in the two chains with a cross-chain currency. With the various cross-chain minerals, liquidity suppliers will simultaneously supply pools of liquidity on two separate chains to integrate liquidity of the tokens on the two different chains.

Ethereum 2.0 is still not the day we are. Nor is Layer 2 ready. Ethereum can, before high gas charges and overcrowded networks are fully solved, be a significant medium for customer and fund attraction in the short run with a vast range of possible customers including BSC and HECO. MDEX has many benefits, being the only DEX that embraces two public chains. Its appealing financial capability comes at the beginning from the dual-mining process and incredibly high APY. These benefits enable MDEX to quickly protect TVL in large volumes. In addition, TVL rapidly grows as well, thanks to the MDX repurchasing & compensation mechanism.

Meanwhile, resolving the HMDX liquidity issue by cross-chain applications would help both BSC and HECO users. Improved liquidity improves the business experience automatically. In its high-liquidity trade pairs, the slip experience of MDEX is higher than other DEX high-liquidity business pairs and has transaction fees such as BSC and HECO.

The combined liquidity of BSC and Heco, strong APY and good user interface both add to MDEX’s 23% market share. The positive for MDEX is the combination of Heco’s liquidity and its customers and its strong transaction mining revenues compared with Pancake. However, minimal product options are also weak. Pancake has a rich portfolio in contrast. In conjunction with products such as IFO and Syrup Pools retail investors will make extensive choices.

AMM goods will in future be more public-oriented. Thus, the emphasis will be on business experience and product simplicity. MDEX has so far been reasonably efficient in data, which lays the groundwork for a certain sector and can become a major advantage in the future. Next, to attract customers and enrich offerings, the MDEX must protect the current TVL benefits.

Source : bscdaily