The Weekly BSC News Newsletter from Kabezo

“That which does not kill us makes us stronger”

— Friedrich Nietzsche on the Fed’s latest rate riseFederal Reserve Chairman Jerome Powell and the rate decision by the U.S. Federal Open Market Committee (FOMC) took center stage as the focus of markets this week. They delivered a 0.75% increase, leaving the Federal Funds benchmark policy rate at 3.25%.

In response to the highest headline inflation indicators since the 1980s, the Fed is tightening credit conditions in a bid to cool demand and price pressures.

During the press conference following the announcement, Powell reiterated his belief that the U.S. economy was running hot, saying “This is a strong, robust economy.”

I hope he is right, but it is not looking good.

U.S. gross domestic product (GDP) was measured at a growth rate of -1.6% and -0.6% in the first two quarters of 2022 respectively. This two-quarter contraction of economic activity meets the definition of a “technical recession,” giving rise to the question of where, exactly, Chair Powell sees strength.

Powell mentioned that the FOMC is forecasting 0.2% GDP growth for 2022, which he acknowledged was well below trend. But considering the contraction in the first half of this year, even that looks overly optimistic.

In response to a question, he said “… the labor market in particular has been very strong.”

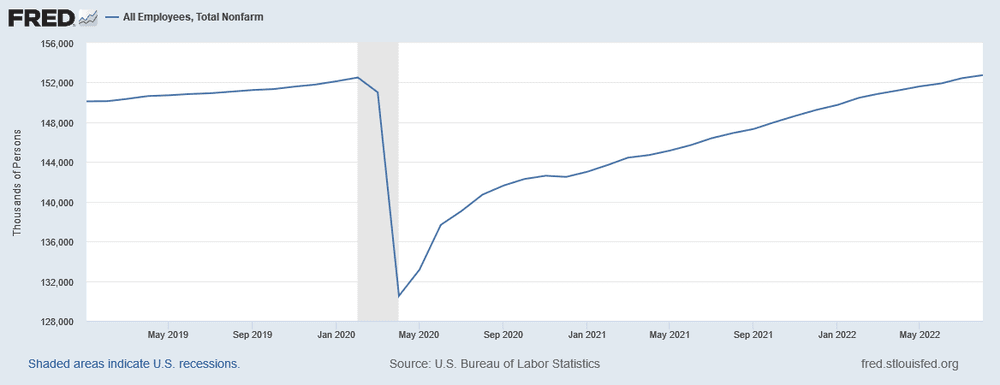

A quick perusal of the FRED database shows that, according to Bureau of Labor Statistics (BLS) data, the U.S. economy only recently recovered the number of jobs lost since the start of the pandemic in January 2020.

Maybe Powell is looking at the unemployment rate, which at 3.7% is low by historical standards. But the fudge with that number is a declining labor force participation rate, which is a full percentage point lower than January 2020 which translates into a loss of 3.3 million jobs. Couple that with a population growth of 1.6 million and … not good.

Powell has access to the FRED database like everyone else. Where does he see this “strong, robust economy” when signs of economic contraction abound?

Commodities are getting smoked. WTI crude oil is below $80 per barrel. Northwest Europe natural gas for winter delivery is still extremely elevated, but well off its highs. There is no panic for U.S. Henry Hub natural gas with the Cal23 strip trading at $5.59. Industrial metals are selling off, such as aluminum which is down 40% from recent highs.

Stock indices are selling off. Both the S&P 500 and the DAX are 24% off their highs, with the NASDAQ 100 down 30%. The Hang Seng index is down 42% from the highs, to levels last traded in 2016.

Surveys of consumer confidence, business sentiment, and purchasing managers are low and trending lower.

As I have often repeated, the U.S. Treasury yield curve is inverted, with the highest rate at the 2-year maturity a full 0.59% higher than the 30-year bond.

This is a very strong signal of recession, confirming what the previous two quarters of GDP contraction have already indicated.

Say It …

I do not envy Powell’s position. He is under pressure to contain rising prices, while hopefully not tanking the economy. Manipulation of short-term interest rates is his main practical tool. But by mentioning “expectations” seven times in the context of inflation during his press conference, he is confirming that managing psychology is an important part of the Fed’s job.

Overnight rates and psychology are the focus, with no mention of the money supply made. Since “Inflation is always and everywhere a monetary phenomenon,” as Milton Friedman famously put it, this appears to be a glaring omission. This is especially so considering signals of monetary contraction are accompanying the economic slowdown.

The U.S. dollar wrecking ball is laying waste to all in its path. The euro is firmly below parity at $0.96. The yen has lost 26% this year, trading at 144 to the dollar, lows not seen since 1998 during the Asian financial crisis. The British pound has lost over 20% to the dollar this year, breaking through levels last seen in 1985, to all-time lows near parity. Emerging market currencies have fared worse.

But perhaps the most vivid evidence of a U.S. dollar shortage is the Chinese yuan. Having broken through the psychologically important level (for the People’s Bank of China) of 7 per dollar, the currency weakness belies the strength of the country’s trade position. The yuan is weakening despite China running up a record-high trade surplus and running down U.S. Treasury holdings down to a 12-year low.

What is the source of this dollar shortage?

The answer is probably something close to a conspiracy theory, or at least a leap of faith: eurodollars. Most overseas funding starts and ends in the eurodollar offshore deposit market. Since it is beyond the purview of the Fed or anyone else, the size and scope of this market is unknowable, except that it is huge.

Attempts to trace the U.S. dollar wreckage stop there. But anomalies like the weakness of the yuan versus the dollar bear the fingerprints of severe tightness in the eurodollar market.

The Fed’s hikes have shifted interest rate curves higher. Despite this, eurodollar futures markets are still forecasting Fed rate hikes to end by June 2023 and for rate cuts to ensue by December 2023.

Darth Gensler

In light of the carnage in TradFi, crypto held up well. BTC managed to hold above the $19K level. The bleeding in ETH appears to have abated at around $1,300. BNB has continued to outperform, holding above the $270 level and up 30% from the July lows.

But clouds are on the horizon as Darth Gensler has reappeared.

A lawsuit brought by the U.S. Securities and Exchange Commission (SEC) has posited a novel legal theory regarding cryptocurrencies. The suit charges Ian Balina, CEO of Tokenmetrics, with conducting an unregistered securities offering in 2018 when SPRK tokens were sold via ICO. In the complaint, the SEC makes explosive (to crypto Twitter) claims about the ICO transactions: “At that point, their ETH contributions were validated by a network of nodes on the Ethereum blockchain, which are clustered more densely in the United States than in any other country. As a result, those transactions took place in the United States.”

Chair Gensler, with all your expertise in crypto, is this really the way you propose to evaluate protocols? Do nodes running the core software of an open protocol need to count the other nodes within the same jurisdiction to avoid securities regulation? What about BTC, where the U.S. also leads the node count?

Is the U.S. aiming to be a leader in this world-changing technology or drive it out of the country completely?

Source : bsc.news

Founded in 2020, BSCNews is the leading media platform covering decentralized finance (DeFi) on the Binance Smart Chain (BSC). We cover a wide range of blockchain news revolving mainly around the DeFi sector of the crypto markets. BSCNews aims to inform, educate and share information with the global investment community through our website, social media, newsletters, podcasts, research, and live ask me anything (AMA). Our content reaches hundreds of thousands of global investors who are active in the BSC DeFi space.

BSC NEWS is a private news network. All posts posted by this user belong 100% to bsc.news All rights are reserved to BSC NEWS for more information about BSC NEWS contact BSC NEWS HERE.